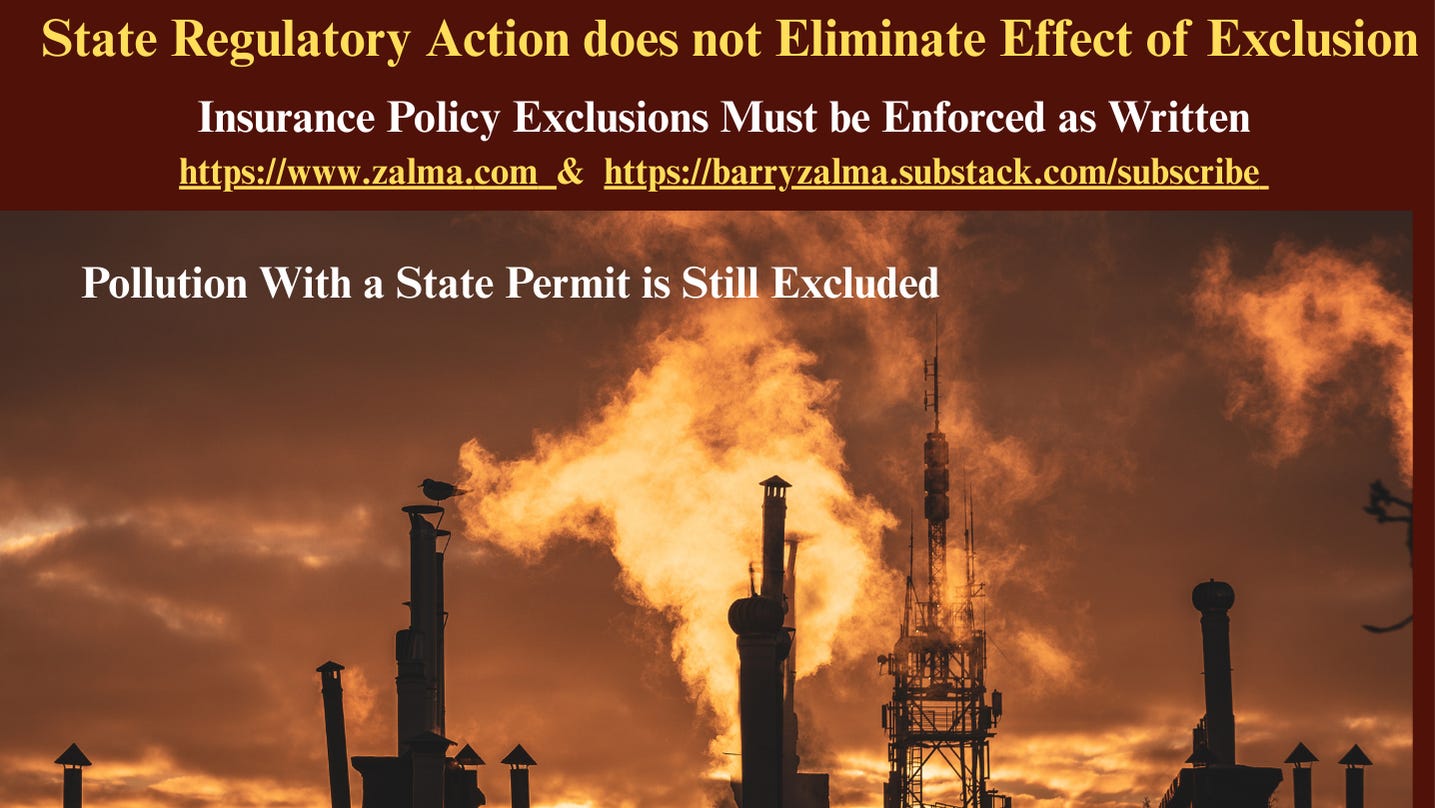

State Regulatory Action does not Eliminate Effect of Exclusion

Insurance Policy Exclusions Must be Enforced as Written

See the video at https://lnkd.in/grQRRWa5 and at https://lnkd.in/gH8gtAr2, and at https://zalma.com/blog plus more than 5250 posts.

Post number 5272

Pollution With a State Permit is Still Excluded

In Griffith Foods International, Inc., et al. v. National Union Fire Insurance Company Of Pittsburgh, Pa, No. 131710, Supreme Court of Illinois, 2026 IL 131710 (January 23, 2026) Griffith Foods International, Inc., and its successor Sterigenics U.S., LLC, operated a medical-equipment sterilization facility in Willowbrook, Illinois. Local residents alleged that for over 35 years, the facility emitted ethylene oxide (EtO), which they claimed caused cancer and other serious illnesses.

The policyholders sought a declaration that National Union Fire Insurance Company of Pittsburgh, PA, was obligated to defend them in the underlying mass tort litigation, based on two CGL policies issued for the facility between September 1983 and September 1985.

The two policies required the insurer to “defend any suit against the insured seeking damages on account of *** bodily injury” that “occur[red] during the policy period” and “personal injury” arising out of “offenses committed during the policy period.” The CGL policies included a standard pollution exclusion, which is the subject of this appeal. The pollution exclusion bars coverage for “bodily injury or property damage arising out of the discharge, dispersal, release or escape of smoke, vapors, soot, fumes, acids, alkalis, toxic chemicals, liquids or gases, waste materials or other irritants, contaminants or pollutants into or upon land, the atmosphere or any water course or body of water.”

THE QUESTION FROM THE SEVENTH CIRCUIT

“In light of the Illinois Supreme Court’s decision in [American States Insurance Co. v. Koloms, 177 Ill.2d 473 (1997)] what relevance, if any, does a permit or regulation authorizing emissions (generally or at any particular levels) play in assessing the application of a pollution exclusion within a standard-form commercial general liability policy?”

LEGAL ISSUE

The key legal issue was the interpretation of the pollution exclusion in the CGL policies, which excludescoverage for bodily injury or property damage resulting from the release of pollutants, including toxic chemicals and gases, into the environment.

ANALYSIS

The Court reasoned that the pollution exclusion is triggered by the nature of the contaminant released and the resulting injury, not by whether the release was authorized or regulated. Past decisions confirmed that the exclusion applies regardless of compliance with permits or regulatory standards. Thus, the presence of a permit or regulation authorizing emissions does not influence the scope or application of the exclusion; coverage is barred so long as the injury results from pollutants as defined in the policy.

OPINION

The Supreme Court of Illinois, responding to the certified question from the Seventh Circuit, held that a permit or regulation authorizing emissions — whether generally or at specific levels — does not affect the interpretation or application of the pollution exclusion clause in a standard-form commercial general liability (CGL) insurance policy. The Court’s answer was clear: such regulatory authorizations are irrelevant when determining coverage under the pollution exclusion.

The plain language of the pollution exclusion states that coverage is barred for litigation involving “the discharge, dispersal, release or escape of smoke, vapors, soot, fumes, acids, alkalis, toxic chemicals, liquids or gases, waste materials or other irritants, contaminants or pollutants into or upon land, the atmosphere or any water course or body of water.”

The fact that the IEPA permitted the EtO emissions does not change this analysis. The pollution exclusion says nothing about permitted or authorized pollution, and courts must not inject terms and conditions different from those agreed upon by the parties.

In addition, the pollution exclusion in CGL policies was drafted in response to the insurance industry’s concerns about increasing, costly environmental litigation. Declining to apply the pollution exclusion simply because the pollution was permitted by the State would undermine the pollution exclusion’s very purpose. In sum, in determining whether the pollution exclusion in a CGL policy applies, the Supreme Court held that it is irrelevant whether the underlying pollution is permitted or not.

CONCLUSION

For the foregoing reasons, the Supreme Court answered the certified question as follows: “a permit or regulation authorizing emissions (generally or at any particular levels) has no relevance in assessing the application of a pollution exclusion within a standard form commercial general liability policy.”

ZALMA OPINION

The Supreme Court of Illinois interpreted the insurance policies as they are written and refused to add language that was not in the policy to provide coverage for the alleged polluters. The polluters claimed having a permit changed the fact that they polluted the atmosphere. No coverage because the exclusion was clear and unambiguous.

(c) 2026 Barry Zalma & ClaimSchool, Inc.

Please tell your friends and colleagues about this blog and the videos and let them subscribe to the blog and the videos.

Subscribe to my substack at https://barryzalma.substack.com/subscribe

Go to X @bzalma; Go to Barry Zalma videos at Rumble.com at https://rumble.com/account/content?type=all; Go to Barry Zalma on YouTube- https://www.youtube.com/channel/UCysiZklEtxZsSF9DfC0Expg;

Go to the InsuranceClaims Library – https://lnkd.in/gwEYk.